DentiPath Learn

How dental associate splits work: 35%, 40%, 45%, and 50% examples

A dental associate split is a percentage used to calculate compensation from a defined pay base, such as production, adjusted production, collections, or another contract-defined amount. A 35%, 40%, 45%, or 50% split does not mean much unless you know what the percentage is applied to and which deductions come first. The same percentage can produce very different income depending on the base and the contract terms.

The examples below are for education only. They are not compensation benchmarks or recommendations. They show how the same headline percentage can produce different estimates once the base, lab fees, and deductions are added.

Want to put numbers to it? The Associate Income Calculator lets you test how different split percentages, production bases, collections, lab fees, and deductions can change an associate income estimate. For saved scenarios and side-by-side offers, DentiPath Finance™ models it privately on your device.

What a dental associate split means

A dental associate split is a percentage in a compensation formula. It is often written as a simple percentage, such as 35%, 40%, 45%, or 50%. But the percentage is only one part of the formula. The full calculation usually depends on the compensation base, the split percentage, the treatment of lab fees, the treatment of write-offs and discounts, the timing of collections, the payment schedule, and any daily minimums, draws, guarantees, bonuses, or clawbacks.

A useful way to think about it is: pay base, times associate split, less deductions, plus guarantees or bonuses. If the pay base changes, the result changes.

Why the pay base matters

A split can be based on different numbers. Common bases include gross production, adjusted production, billable production, collections, net collections, production after lab fees, collections after lab fees, and net profit or another contract-defined amount.

Take one example. An associate has gross production of $90,000, adjusted production of $78,000, and collections of $74,000 in a month. A 40% split produces different results depending on the base.

| Pay base | Amount | Split | Estimate |

|---|---|---|---|

| Gross production | $90,000 | 40% | $36,000 |

| Adjusted production | $78,000 | 40% | $31,200 |

| Collections | $74,000 | 40% | $29,600 |

The percentage is identical. The result is not.

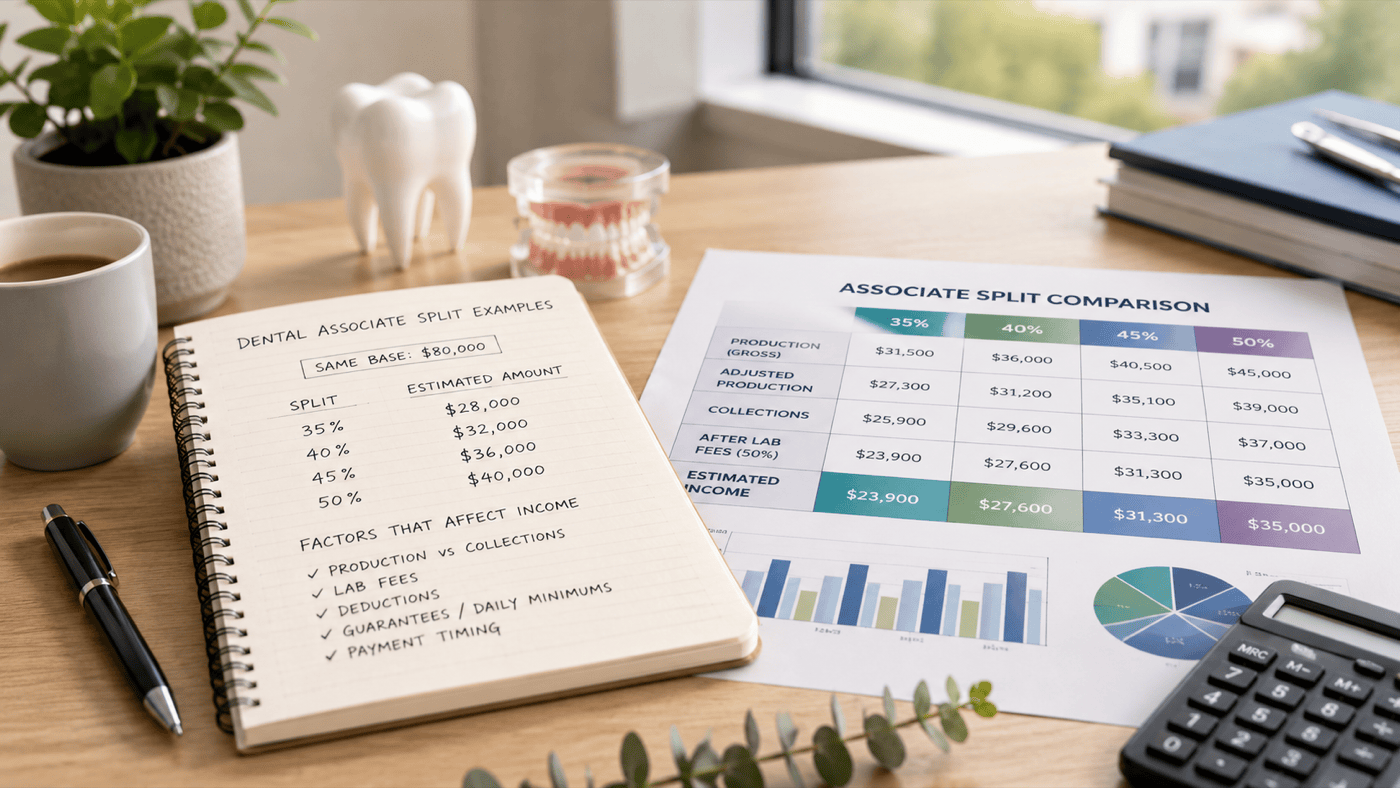

Example 1: 35%, 40%, 45%, and 50% on the same production base

Start with a simple case. Assume the compensation base is $80,000, with no extra deductions. Now compare four split percentages.

| Split | Calculation | Estimated amount |

|---|---|---|

| 35% | $80,000 times 35% | $28,000 |

| 40% | $80,000 times 40% | $32,000 |

| 45% | $80,000 times 45% | $36,000 |

| 50% | $80,000 times 50% | $40,000 |

This is the cleanest version of split math. If the base is the same and there are no extra deductions, a higher percentage produces a higher estimate. But real contracts are often more complicated.

Example 2: a higher split on collections can be lower than a lower split on adjusted production

Now compare two offers. Offer A is 35% of adjusted production on a base of $80,000. Offer B is 40% of collections on a base of $65,000.

| Offer | Base | Split | Calculation | Estimate |

|---|---|---|---|---|

| Offer A | Adjusted production $80,000 | 35% | $80,000 times 35% | $28,000 |

| Offer B | Collections $65,000 | 40% | $65,000 times 40% | $26,000 |

Offer B has the higher percentage, but Offer A produces the higher estimated amount in this example. This does not mean adjusted production is always better. It means the base matters.

Example 3: lab fees can change the real value of the split

Lab fees can materially affect associate compensation when the contract shares or deducts them. This matters especially for crowns, bridges, implants, aligners, dentures, and other lab-supported procedures.

Assume collections of $80,000, lab fees of $8,000, and associate lab fee responsibility of 50%. The associate’s share of lab fees is $8,000 times 50%, which is $4,000. Now compare four split percentages.

| Split | Amount before lab share | Lab fee share | Estimated amount after lab share |

|---|---|---|---|

| 35% | $28,000 | $4,000 | $24,000 |

| 40% | $32,000 | $4,000 | $28,000 |

| 45% | $36,000 | $4,000 | $32,000 |

| 50% | $40,000 | $4,000 | $36,000 |

The lab fee treatment does not change the headline percentage, but it changes the final estimate.

Example 4: deducting lab fees before the split

Some contracts may deduct lab fees from the compensation base before applying the split. Assume collections of $80,000 and lab fees of $8,000, which gives a lab-adjusted base of $72,000. Now compare four split percentages.

| Split | Calculation | Estimated amount |

|---|---|---|

| 35% | $72,000 times 35% | $25,200 |

| 40% | $72,000 times 40% | $28,800 |

| 45% | $72,000 times 45% | $32,400 |

| 50% | $72,000 times 50% | $36,000 |

This may look similar to subtracting a separate lab share, but the math can differ depending on the contract. The contract should define exactly how lab fees are handled.

Example 5: a lower split with stronger collections can beat a higher split with weaker collections

Assume two practices have the same gross production of $90,000, but different collections. Practice A collects $82,000 at a 35% split. Practice B collects $70,000 at a 40% split.

| Practice | Collections | Split | Calculation | Estimate |

|---|---|---|---|---|

| Practice A | $82,000 | 35% | $82,000 times 35% | $28,700 |

| Practice B | $70,000 | 40% | $70,000 times 40% | $28,000 |

Practice B has the higher split, but Practice A produces the higher estimate in this example. This is why collection rate, payer mix, billing systems, and patient payment processes matter when evaluating a collections-based offer.

What can make two splits hard to compare

Two offers can be hard to compare if they differ in more than one variable. For example:

| Variable | Offer A | Offer B |

|---|---|---|

| Split | 35% | 40% |

| Base | Adjusted production | Collections |

| Lab fees | No deduction | 50% associate share |

| Daily minimum | Yes | No |

| Schedule | 4 days/week | 5 days/week |

| Patient flow | Established | Ramp-up needed |

| Benefits | Included | Not included |

| Reconciliation | Monthly | Quarterly |

In this kind of comparison, the split percentage alone is not enough. You need to model the full offer.

Questions to ask about a split-based offer

Before comparing split percentages, ask:

- Is the split based on production, adjusted production, collections, or another number?

- Does the contract define the pay base clearly?

- Are lab fees deducted before or after the split?

- Are lab fees shared separately?

- Are write-offs, discounts, refunds, or remakes deducted?

- Are certain procedures excluded?

- How often is compensation reconciled?

- Are reports available for associate-level production and collections?

- Is there a daily minimum, guarantee, or draw?

- Do deficits carry forward?

- Are bonuses discretionary or formula-based?

- What happens to unpaid collections after departure?

Worked example: four split structures on the same monthly scenario

Assume a hypothetical associate has gross production of $90,000, adjusted production of $78,000, collections of $74,000, monthly lab fees of $6,000, and associate lab fee responsibility of 50%. Now compare four structures.

| Scenario | Structure | Calculation | Estimated amount |

|---|---|---|---|

| Scenario A | 35% of adjusted production, no lab fee deduction | $78,000 times 35% | $27,300 |

| Scenario B | 40% of collections, no lab fee deduction | $74,000 times 40% | $29,600 |

| Scenario C | 45% of collections, with 50% lab fee share | $33,300 less the $3,000 lab share | $30,300 |

| Scenario D | 50% of lab-adjusted collections | $68,000 times 50% | $34,000 |

For Scenario C, the amount before the lab share is $74,000 times 45%, which is $33,300; the lab share is $6,000 times 50%, which is $3,000; and the estimate is $33,300 less $3,000, which is $30,300. For Scenario D, the lab-adjusted collections are $74,000 less $6,000, which is $68,000; the estimate is $68,000 times 50%, which is $34,000.

In this example, the highest percentage produces the highest estimate, but that will not always be true. If collections, lab fees, patient flow, or deductions change, the ranking can change.

Key takeaway

A dental associate split is not just a percentage. It is a percentage applied to a defined base, often with deductions, timing rules, and contract-specific adjustments. Before comparing 35%, 40%, 45%, or 50% offers, identify the pay base, the split percentage, the deduction rules, the timing of reconciliation, the expected production and collections, the lab fee treatment, and any daily minimum or guarantee. The strongest offer is not always the one with the highest percentage.

Test a few scenarios with the Associate Income Calculator before comparing offers.

Keep reading

Model your own numbers privately.

DentiPath Finance™ saves full compensation scenarios and compares two offers on the same basis; DentiPath Ledger™ tracks what actually lands. Both private, on-device, and account-free.

Questions

What is a dental associate split?

A dental associate split is a percentage used to calculate compensation from a defined pay base, such as production, adjusted production, collections, or another contract-defined amount.

Is a higher split always better?

No. A higher split can produce less income if it is applied to a lower base or reduced by larger deductions. The full formula matters more than the percentage alone.

Is 40% better than 35%?

Not necessarily. A 35% split on adjusted production can produce more than a 40% split on lower collections, depending on the numbers.

How do lab fees affect a split?

Lab fees can reduce associate compensation if the contract deducts them before the split, shares them separately, or subtracts them from the associate’s calculated amount. The exact effect depends on the contract.

Should I compare splits monthly or annually?

Both can be useful. Monthly modelling helps show short-term cash flow, while annual modelling helps compare the broader value of different offers.

Should I review a split-based contract with a professional?

Yes. Split-based compensation can interact with contract terms, worker status, tax treatment, lab fee deductions, restrictive covenants, and exit provisions. This article is educational and does not replace professional review.

Method and sources

- American Dental Association dentist compensation guidance: compensation structures and contract questions.

Start with the app that matches where you are.

Free to download. On your device, no account required.

Research and verification

How this resource is supported

Research frame

Calculate illustrative percentage scenarios from a clearly defined pay base, lab fee rule, adjustment rule, and payment period.

Boundaries to verify

Examples do not establish a standard market percentage. Taxes, benefits, and contract deductions may change take-home pay.

Official sources

- Dentists Tax and Financial Guide Ontario Dental Association

- Employee or Self-employed? Canada Revenue Agency

- Payment of wages Government of Ontario

DentiPath Learn is for educational and personal planning purposes only. It is not financial, legal, tax, accounting, employment, or clinical advice. Compensation structures, worker status, tax treatment, and contract terms vary by jurisdiction and by the facts of the working relationship. Calculations are estimates based on user-entered values. Review contracts and financial decisions with qualified local professionals before relying on any model or signing an agreement.